For owners of high-end brands like Porsche, Mercedes-Benz, and BMW, an accident causes a sharp drop in market value that repairs cannot fix. This is a significant financial hit, and knowing how to prove diminished value is the only way to protect your investment.

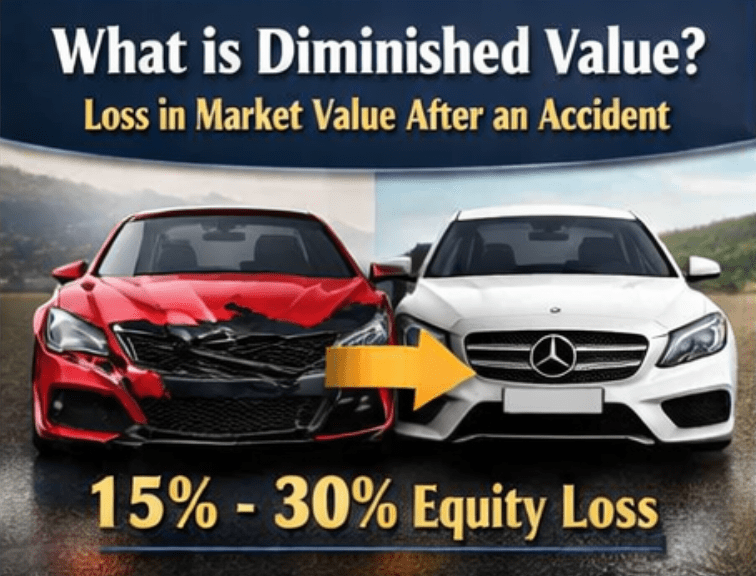

This difference between the pre-accident value and the post-repair value is known as Diminished Value. For luxury vehicles, a single accident can result in a 15% – 30% equity loss. As a owner, you have the legal right to recover this loss of value insurance car claim from the at-fault party.

I. Core Definition: Why “Repaired” Does Not Mean “Made Whole”

Diminished Value is the gap between what your car was worth before the accident and what it is worth now that it has a damage history.

- Identify Your Claim Type

- Third-Party Claim (Against the At-Fault Insurance): The most common route. If the other party is entirely or primarily at fault, you should file a claim against their insurance provider.

The Challenge: Insurance companies rarely offer this automatically. You must understand how to get diminished value from insurance companies who are trained to minimize payouts.

- First-Party Claim (Against Your Own Insurance): Generally difficult to recover unless your specific policy includes a “Diminished Value” endorsement.

- The Three Dimensions of Value Loss

- Inherent Diminished Value (The Core Loss): The loss of value simply because the vehicle history report (e.g., Carfax) now shows an accident, leading to “market stigma” and buyer distrust.

- Repair-Related Diminished Value: Additional loss caused by repair imperfections, such as paint mismatch, uneven panel gaps, or the use of non-OEM parts.

- Immediate Diminished Value: The drop in the vehicle’s resale value at the moment of impact, before repairs even begin.

II. 5 Key Factors Affecting Luxury Diminished Value

Insurance adjusters determine your payout based on the following criteria:

- Severity of Damage: Structural damage (chassis, frame, or rails) results in much higher depreciation than simple cosmetic paintwork.

- Quality of Repair & Parts: While using OEM (Original Equipment Manufacturer) parts is essential, the complex craftsmanship of luxury cars means any non-factory repair signature is viewed as a major flaw by the market.

- Brand, Model, and Year: The more expensive, newer, or rarer the vehicle, the more sensitive it is to devaluation.

- Pre-Accident Condition: A vehicle that was in “showroom condition” with a perfect record will suffer a more devastating drop in value than a poorly maintained one.

- Market Stigma (Psychological Discount): Luxury buyers are extremely sensitive to accident history. This psychological price barrier is the driving force behind high-end claims.

III. Evidence Collection & Documentation

Luxury claims require rigorous objective data. To succeed in your claim, you must answer the primary question: how do you prove diminished value effectively?

Phase 1: At the Scene & Pre-Repair (Immediate Action)

- Comprehensive Documentation: Take time-stamped photos of the original damage from multiple angles. Obtain the Police Report to confirm liability.

- Insist on Certified Repairs: Ensure the vehicle is repaired at a Brand-Authorized Certified Collision Center to maintain a verifiable paper trail.

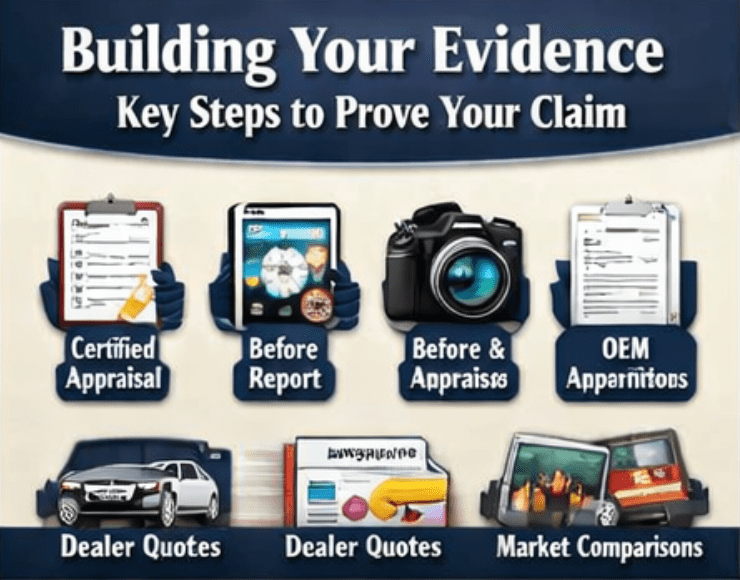

Phase 2: Building the Luxury Evidence Chain (Crucial)

Luxury claims require rigorous objective data. Do not rely on oversimplified online calculators. You need high-strength evidence:

- ✅ Professional Certified Appraisal Report: Prepared by an independent appraiser. This is your primary legal-grade evidence on how to prove diminished value.

- ✅ Vehicle History Report Comparison: Provide “Before and After” Carfax or AutoCheck reports to prove the accident is now a permanent stain on the car’s pedigree.

- ✅ High-Definition “Before & After” Photos: Original damage photos contrasted with detailed post-repair shots to objectively assess how the damage affected the vehicle’s integrity and final aesthetics.

- ✅ OEM Repair Invoices: A detailed itemization proving all parts used were original factory components, with zero aftermarket substitutions.

- ✅ Dealer Quote for Trade-in: Obtain 2–3 written valuations from authorized dealers explicitly stating: “How much more the car would be worth if it did NOT have this accident history.”

- ✅ Market Comparison Analysis (Comps): A data set showing the actual sale prices of identical “clean title” vehicles versus those with similar accident records.

IV. Calculation, Submission, and Negotiation Strategy

1.Calculation Logic

The standard process: Determine Fair Market Value (Pre-Accident) ➔ Apply Depreciation Multiplier based on damage severity ➔ Adjust for mileage.

2.Submitting the Demand Letter

Your Demand Letter must be professional, detailing the accident facts and attaching all evidence. This is the first formal step in how to get diminished value from insurance.

3.Negotiation & Countering Denial

- Reject the First Offer: The initial offer from an insurance company is almost always a low-ball “tester” figure.

- Counter with Data: Use your professional appraisal and dealer quotes to directly challenge the insurance company’s oversimplified internal models.

- Demand a Written Reason for Denial: Force the adjuster to provide a formal response. This creates a trail for potential complaints to the State Department of Insurance.

- Follow Up Persistently: Do not show a willingness to settle cheaply. The more professional your evidence, the harder it is for them to deny the claim.

V. Common Mistakes & Risk Mitigation

- ❌ Signing a Release Too Early: Never sign a “Full Release” or “Waiver” until you have received the Diminished Value settlement.

- ❌ Missing the Statute of Limitations: Every state has a deadline (e.g., 3 years in California). Initiate your claim as soon as repairs are complete.

- ❌ Relying on Online Valuation Tools: Generic data fails when explaining how do you prove diminished value for a rare or high-end vehicle.

VI. When to Hire an Attorney?

In legal disputes, courts value objective data over subjective opinions. In the following scenarios, an attorney can significantly increase your recovery:

- High-Value Loss: When the estimated loss of value insurance car exceeds $10,000.

- Liability Disputes: When the at-fault insurance tries to shift or mitigate blame.

- Bad Faith/Hard Denial: When the insurance company refuses to acknowledge a certified appraisal or credible dealer quotes.

- Pre-Settlement Review: Before signing any final settlement agreement.

VII. Post-Settlement File Management

- Audit Settlement Documents: Ensure the payment amount matches the agreed terms in the paperwork.

- Archive the Vehicle File: Keep the appraisal, repair invoices, HD photos, and settlement proof in both digital and hard-copy formats.

- Resale Transparency: This complete evidence chain will help you prove “repair transparency” to a future buyer, mitigating their concerns and protecting the remaining equity in your asset.

🛡️ Protect Your Asset’s Value Today

Proving diminished value for a luxury vehicle is a systematic undertaking requiring strategy, evidence, and persistence.

👉 [Contact Us: Get Your Exclusive Luxury Diminished Value Appraisal]

👉 [Consultation Hotline: 3105975383]